Last month, lawmakers in Massachusetts approved a constitutional amendment that will lead to the departure of many of the state’s wealthiest and most productive citizens. This move is likely to cause tax revenues to drop and real estate values to collapse.

The proposed change imposes a 4% surtax on residents with taxable income of $1 million or more. Currently, the state income tax rate is a flat 5.1%. So, when the measure comes into effect in 2019, the wealthiest taxpayers in Massachusetts will see their state income tax burden nearly double, which will cause many of them to move elsewhere.

Before the surtax comes into effect, it must be endorsed at a constitutional convention and approved by state voters. But judging by the lopsided votes for approval in both chambers of the legislature, the amendment being passed seems a foregone conclusion. The state Senate voted 33–7 in favor of it; the House vote was 102–50.

Why would seemingly intelligent elected officials enact a law that is almost certain to result in a lower standard of living for Massachusetts residents? Supporters claim it will raise $1.9 billion annually for education and transportation funding. But based on past experience, this seems unlikely.

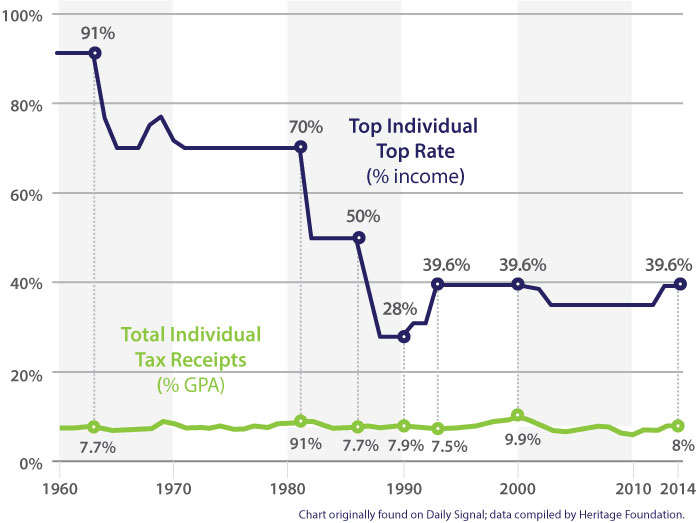

Just look at this graph, which compares the top federal income tax rate to the percentage of GDP of tax collected from individuals. As you can see, despite huge variations in the top rate, total revenue from individual taxpayers has remained remarkably stable over the past 50 years.

Keep in mind that US taxpayers pay the same amount of federal income tax no matter where they live in the US. With one very narrow exception, the only way for US taxpayers to reduce their federal income tax burden is to relocate to another country and give up their US citizenship.

But when states hike taxes, the situation is very different. Residents of states with high taxes don’t need to give up US citizenship to reduce their tax burden. They merely need to move to a state with lower taxes. That’s a big reason why Texas and Florida – states with zero income tax – have the fastest growing populations in the US.

It’s no wonder why one Massachusetts resident – a client of ours – told me that the state should rename itself “Taxachusetts.” Our client, whom I’ll call “Joe,” told me he’s in the process of relocating his family and business to Florida, a state with no income tax. His multi-million-dollar home is already on the market. He’s laid off most of his employees. And according to Joe, many of his wealthy friends will do the same.

Advocates of tax hikes often claim low taxes starve governments of the resources they need. In reality, the opposite is true. Since 2003, annual Massachusetts government expenditures have increased from $23 billion to more than $38 billion. This 65% increase is more than double the cumulative inflation rate of 30.6% during those years.

There’s a widespread belief, especially on the Left, that low taxes are somehow immoral, because fewer resources are available to meet the needs of the poor. But as we’ve already seen, higher taxes won’t lead to higher tax revenues. By imposing a millionaire’s surtax, Massachusetts will likely have fewer dollars available to help its poorest residents.

Economists are virtually unanimous in their conclusion that higher tax rates discourage work, entrepreneurship, and capital formation, and increase poverty. Lower tax rates, on the other hand, encourage these desirable outcomes and reduce poverty.

Another argument for higher taxes is that by extracting more resources from the “rich,” governments can reduce inequality. President Obama has made this argument himself, in lobbying Congress for higher capital gains taxes. In an ABC interview, he explains: “I would look at raising the capital gains tax for purposes of fairness.”

Personally, I’d prefer a different outcome – one that increases wealth across the board. That means lower, not higher, taxes.

Which do you choose?

Mark Nestmann

Nestmann.com