Navigating Foreign Real Estate Investments in Your Self-Directed IRA

-

Written by Brandon Roe

Written by Brandon Roe - Reviewed by Mark Nestmann

-

Updated: April 22, 2025

Updated: April 22, 2025

Contents

- What is a Self-Directed IRA?

- Benefits of Self-Directed IRAs

- Why Place Foreign Real Estate in Your IRA?

- What you need to know before putting real estate in an SDIRA

- IRS Rules

- Local laws may restrict foreign ownership

- Watch out for UBIT

- The Role of the Custodian

- The Custodian's Perspective

- Common Mistakes in Foreign Real Estate IRAs

- Who Can Benefit Most from an SDIRA Holding Foreign Real Estate?

- Understanding Foreign Real Estate Risks

- Frequently Asked Questions

- Need some help?

Individual Retirement Accounts (IRAs) are a big part of many American investment plans – to the tune of about $13 trillion in 2021.

Most of that is stored in US stocks, bonds, mutual funds and, more recently, Bitcoin.

Planning to Buy Property Abroad? Start Here.

Before you sign anything overseas, make sure you know what you’re doing.

Our most popular expert resources – on structuring, taxation, legal pitfalls, and due diligence – are yours, free.

The Nestmann Group does not sell, rent or otherwise share your private details with third parties. Learn more about our privacy policy here.

By signing up for this briefing, you’ll also start to receive our popular weekly publication, Nestmann’s Notes. If you don’t want to receive that, simply email or click the unsubscribe link found in every message.

But the truth is, IRAs are wonderfully flexible tools. They can hold all sorts of assets including one of much interest to our audience – foreign real estate.

In this article, we’ll talk about why your current IRA custodian likely won’t let you invest in foreign real estate, what’s needed to “open up” your IRA, and how to get started.

What is a Self-Directed IRA?

A self-directed Individual Retirement Account (SDIRA) is a type of IRA that lets you invest in a wider range of assets than most “normal” IRAs allow – stocks, bonds, mutual funds, and maybe Bitcoin.

A self-directed IRA can include all sorts of investments – some forms of precious metals, private companies, domestic real estate, and foreign real estate.

Self-directed IRAs offer the same tax benefits as other IRAs. Up to a certain yearly limit, contributions to self-directed traditional IRAs are tax-deductible. Most earnings grow tax-deferred until withdrawal. At that time, they’re taxed as ordinary income at a top rate of 37%.

If you create or convert to a self-directed Roth IRA, you don’t get a tax deduction up-front, but you do enjoy the gains from assets in the plan tax-free.

Investors make all the investment decisions and must use an IRS-approved custodian to hold the assets. This custodian manages the account and handles the transactions but does not give investment advice or assess potential investments.

Self-directed IRAs are ideal for those wanting to expand their retirement portfolios beyond traditional securities or who have expertise in other investments.

But it’s essential for investors to know and follow IRS rules about prohibited transactions and interactions with disqualified persons. Staying compliant avoids loss of the IRA’s tax and asset protection benefits.

Avoiding Prohibited Transactions in Your IRA

Self-directed IRAs are a great way to build up retirement savings. But it comes with the risk of prohibited transactions. Here’s how to avoid these: self-directed IRA prohibited transactions.

Benefits of Self-Directed IRAs

The biggest advantage with self-directed IRAs is the control it gives you over your investments.

Traditional IRAs typically limit investments to stocks, bonds, and mutual funds. Maybe some crypto.

Self-directed IRAs allow a broader range of options by contrast. This can include all sorts of assets such as private placements, some forms of precious metals, tax lien certificates, and real estate.

Even better, these assets can be held domestically and internationally.

Why Place Foreign Real Estate in Your IRA?

There are several reasons to consider adding foreign real estate to your IRA. As we covered in an article dedicated to foreign real estate investment, they include:

- Diversification Benefits: Investing in property in different countries can make your investment safer. It helps balance your risk during tough times in any one market.

- Potential for Higher Returns: Buying property in places that are growing fast, like certain cities in Asia and South America, can earn you more money from rents.

- Market Growth Opportunities: As more people move to cities and populations grow in certain parts of the world, the demand for homes and shops increases. This can increase the value of properties you invest in these areas.

- Currency Advantage: When the US dollar is strong, you can buy properties in other countries for less money. If the dollar value drops later, your overseas property can be worth more in dollars.

- Leverage of Local Economies: Investing in areas with strong job growth or lots of tourists can pay off well. These areas tend to do better than other places.

What you need to know before putting real estate in an SDIRA

Before investing in real estate overseas with a self-directed IRA, it’s important to know the rules and regulations around them. Let’s talk about some of the most important ones.

IRS Rules

The IRS has rules for using IRAs to buy real estate, both in the US and other countries.

For example, if you use your IRA-owned property for personal reasons (or allow relatives to do so), it will be considered a “prohibited transaction” and trigger full taxation on the entire value of the IRA at your marginal rate (as high as 37%). If you are younger than 59½, you’ll also face a 10% penalty for taking the money out early.

Local laws may restrict foreign ownership

Many countries have restrictions on direct foreign ownership of real estate. Setting up a structure within those jurisdictions may facilitate investment while adhering to local laws.

For example, in Mexico, the “Fideicomiso” system allows a Mexican bank to hold the legal title to the property on behalf of the foreign buyer, structured through a Mexican trust. [Here you can find more information on buying property in Mexico.]

Watch out for UBIT

Investments in real estate through an IRA can also bring up issues related to something called Unrelated Business Income Tax (UBIT). Basically, if your real estate is financed through debt, the debt financed portion of the income or gains is subject to UBIT, where you’ll be taxed at greatly condensed brackets.

For 2024, the top UBIT bracket (37%) applies to such income above $15,200 annually.

There are additional rules relating to borrowing money to finance an IRA investment that can lead to a prohibited transaction.

The Role of the Custodian

Every IRA needs a custodian who’s legally obligated to oversee your IRA within the boundaries of the law. In a traditional setup, the person selling you the investments serves this role. But with an SDIRA, you must find a third-party company who will take on your account.

Serving as a custodian is risky, especially with SDIRAs. Because of this risk, not all SDIRA custodians will give you access to the full range of investments IRAs are allowed to hold. So you’ll need to shop around to find one that will play this role for the investments you want.

Experience and expertise are also important here. Make sure the custodian has a solid understanding of the rules for UBIT and prohibited transactions.

The Custodian's Perspective

When you have a self-directed IRA and invest in things like foreign real estate, your custodian fulfills an important role. They must follow the law very closely to make sure everything in your IRA is handled the right way. They have a fiduciary responsibility to look out for your best interests.

Since making a mistake can lead to big fines or other serious problems for your IRA, custodians are usually very conservative.

Custodians also work hard to protect your investment. They can be obsessed with documentation and due diligence because they are required to keep detailed records and handle all the paperwork needed to stay on the right side of IRS rules.

Common Mistakes in Foreign Real Estate IRAs

When investing in self-directed IRAs (SDIRAs) with foreign real estate, here are some common mistakes to avoid:

Improper Expense Management

It’s important to use the IRA funds to cover all property-related expenses like repairs, taxes, and insurance. Using personal funds for these expenses is a prohibited transaction that can blow up your entire IRA. In most cases, every dollar in the IRA will be subject to income tax at a top rate of 37%. If you’re under 59½, there will also be an extra 10% early distribution penalty.

Unauthorized Use of Property

The property cannot be used by the IRA owner, their family, or close associates. Doing so results in a prohibited transaction, again resulting in a deemed distribution of the entire IRA.

Local Ownership Issues

Understanding the ownership laws in foreign countries is crucial, especially around issues of probate. Potential double taxation can be a problem too in some places.

UBIT Issues

If your IRA borrows money to buy a property, the debt-financed portion of the income or gain is subject to UBIT.

Violating IRS Rules

Engaging in transactions that benefit the IRA owner or related persons, like renting to a family member, will result in a prohibited transaction and the deemed distribution of the entire IRA.

Tax Reporting Errors

Accurate reporting of the value of foreign real estate in an IRA is mandatory. Mistakes in reporting can lead to significant penalties.

Not Following Local Regulations

Each country has its own rules about property ownership and taxes. Ignoring these can lead to financial losses and legal issues.

Poor Choice of Custodian

Choosing a custodian without enough expertise in the rules for UBIT and prohibited transactions can risk fines, penalties, or even the deemed distribution of your entire IRA.

Having Too Little Liquidity after Age 73

Starting at age 73, you must begin taking required minimum distributions from a traditional IRA. If you have too much real estate (or any illiquid asset) and you have to start taking mandatory distributions, you could end up in a situation where you have to sell your property at a fire sale price to be able to pay the tax on that distribution.

Before You Buy Overseas Property

Avoid costly mistakes in international real estate. Learn the 8 key pitfalls and how to navigate them successfully here: pitfalls of international real estate.

How to Finance Foreign Real Estate as an American

We’ll break down the financing options that worked for our clients. From developer financing to cross-border loans, here’s how to finance foreign real estate.

Who Can Benefit Most from an SDIRA Holding Foreign Real Estate?

Not everyone is the right fit for this strategy. Here are a few sample types of ideal clients.

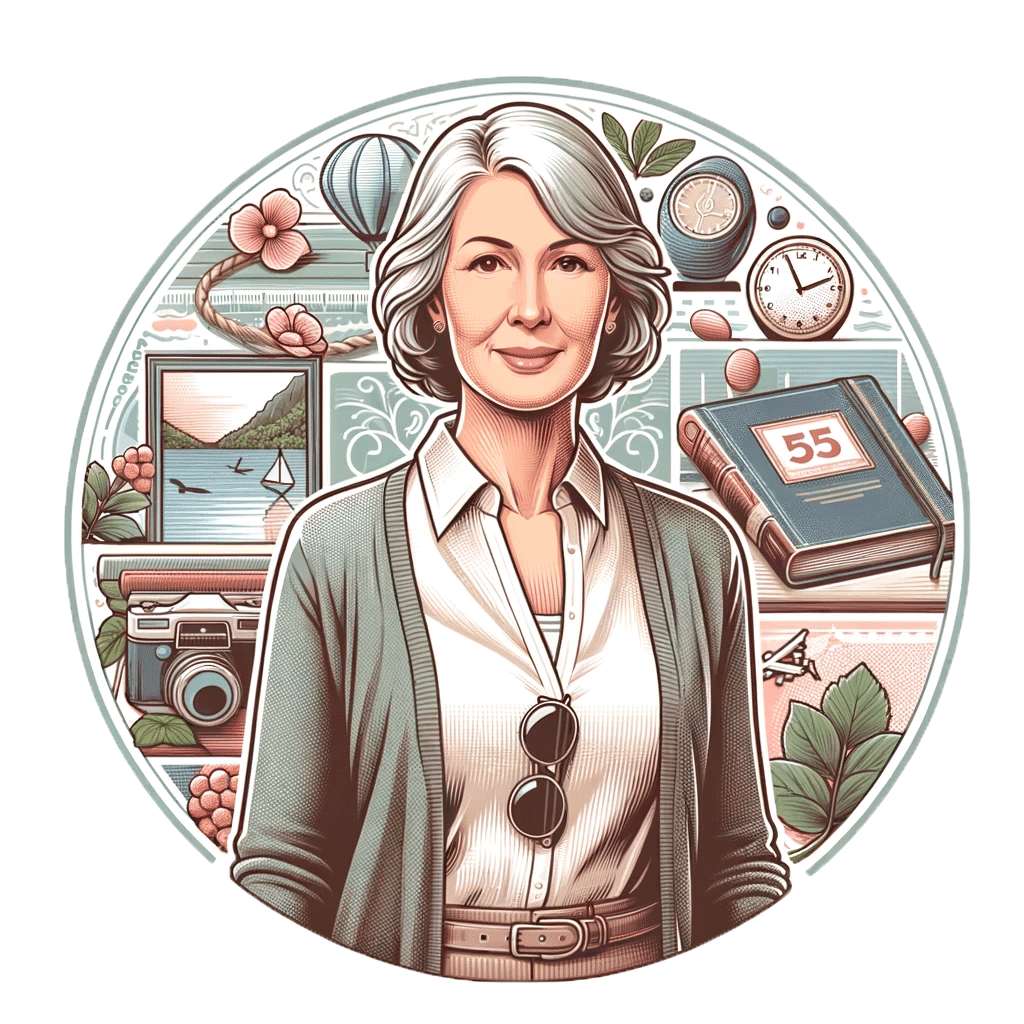

Retirement Diversification

Kelly is a corporate executive in her mid-fifties who has spent her career working for a multinational company. She has a balanced portfolio of stocks and bonds. But she is increasingly interested in securing her future. She wants protection against market swings and economic downturns.

Investment Philosophy: Kelly is a fan of diversification beyond the usual financial instruments. She is keen on exploring alternative investments that offer both growth and stability as she moves closer to retirement.

Goals: Kelly’s main goal is to diversify her retirement funds. She wants to add assets that are not tied to the US. She sees foreign real estate as a way to achieve geographical and currency diversification.

Strategy: Kelly uses a self-directed IRA to buy a residential property in an emerging market country. She anticipates that the property will not only generate rental income, but also appreciate in value. This adds security to her retirement savings.

NOTE: We have changed the case details to preserve client privacy.

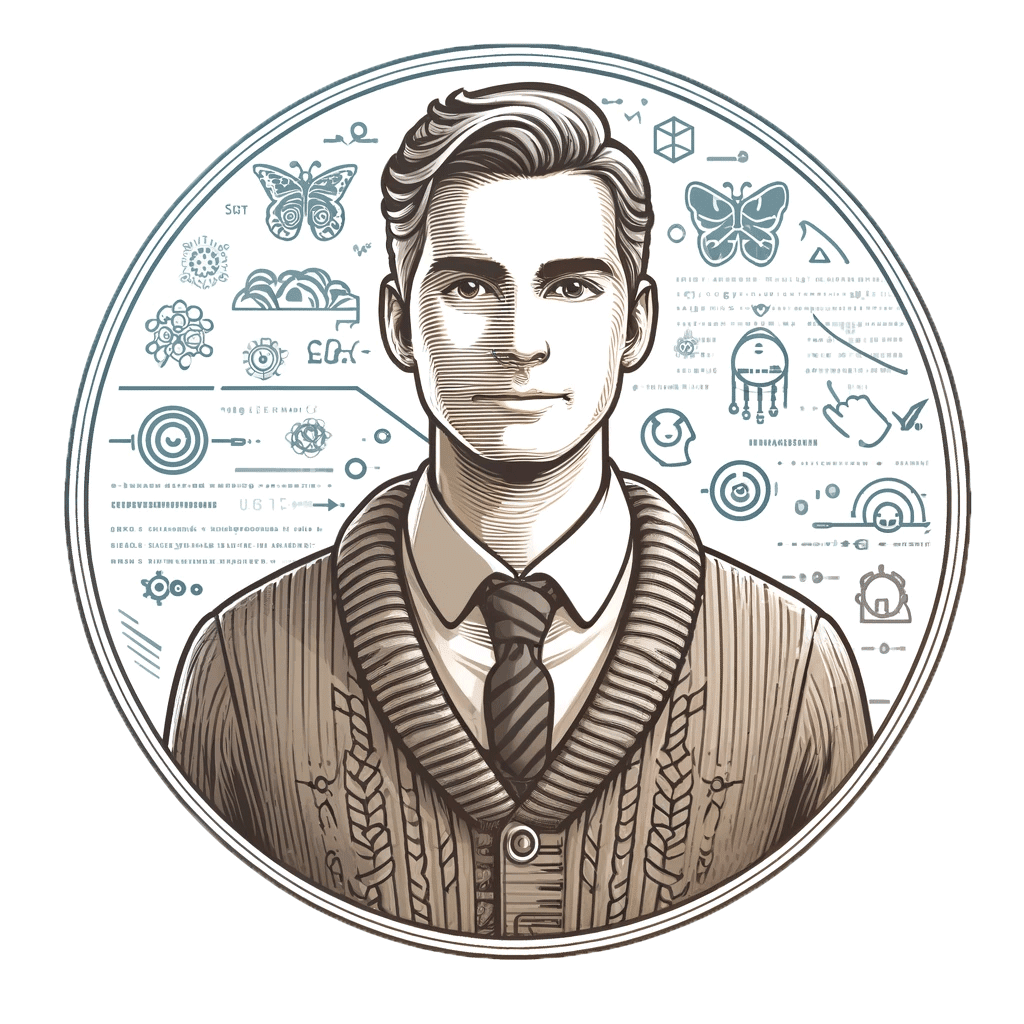

Expat Investors

Peter is a software engineer in his late forties from California who has spent significant time living and working in Europe and Asia. He likes Italy and plans to retire to the countryside there.

Investment Philosophy: Peter focuses on investments that can serve dual purposes—financial return and personal utility. He is particularly interested in real estate markets where he has personal knowledge and connections.

Goals: Peter’s goal is to invest in a property that can serve as a retirement home while also potentially providing rental income in the years leading up to his retirement.

Strategy: Using a self-directed IRA, Peter buys an apartment in Italy and rents it out on Airbnb Once he retires, he will distribute the property in the IRA to himself at which time he can legally reside in it without risking a prohibited transaction.

NOTE: We have changed the case details to preserve client privacy.

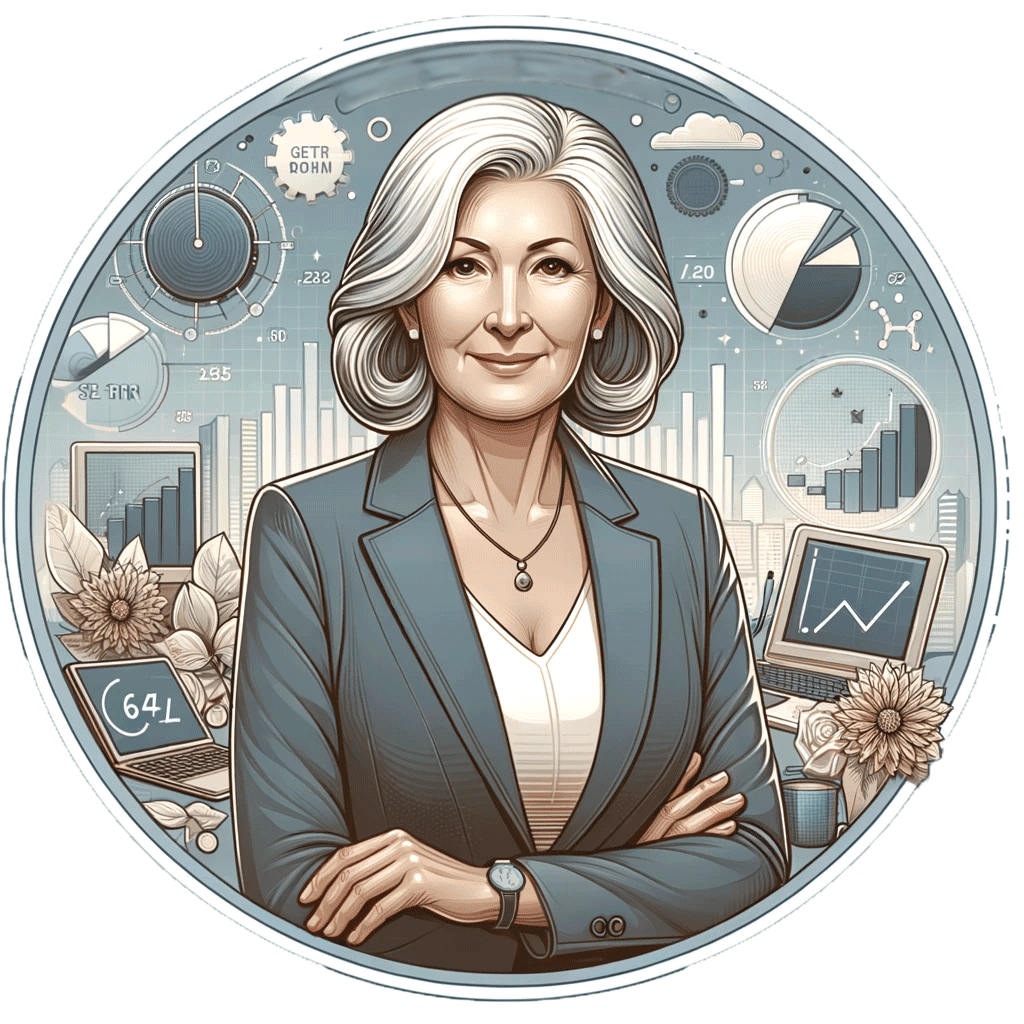

High Net Worth Individuals (HNWIs)

Edna is in her early sixties and from Michigan. She is an entrepreneur who built a successful technology startup and has diverse investments in the US, Canada and Europe. She also always looks for new investment opportunities.

Investment Philosophy: Edna is a savvy investor and understands compliance and regulatory issues that come with being an American investing internationally. She is particularly drawn to investments that offer long-term growth, tax efficiency, and asset protection.

Goals: Edna wants to include international real estate for asset diversification, asset protection, and a Plan B scenario.

Strategy: Edna decides to use her self-directed IRA to invest in commercial real estate in Ireland. She will structure these investments through a local company to block UBIT.

NOTE: We have changed the case details to preserve client privacy.

Understanding Foreign Real Estate Risks

Like any international investment — whether through a self-directed IRA or otherwise — it’s important to be aware of the risks. Here are the biggest ones:

Market Risks

Foreign real estate markets can be more volatile than US markets. Political instability, economic downturns, or changes in government policy can greatly affect property values. This is especially true with smaller, less well-regulated countries.

Regulatory Risks

Each country has its own laws and regulations about foreign ownership of real estate, that are often unfamiliar to US clients. Non-compliance can lead to fines, penalties, or even the loss of property in extreme cases.

Foreign Tax Risks

Income or gain within an IRA is generally tax-deferred according to US tax rules. But a foreign country will apply its own tax rules when it comes to real estate within its borders. In most cases, your IRA will need to pay tax on such income or gain, despite being tax-deferred in the US.

Probate Risks

Some countries – especially civil law countries like Panama, Costa Rica, and much of Europe – have long, drawn-out and expensive probate processes after an owner (or joint owner) passes.

Currency Exchange Risks

The currency in which a foreign investment is valued can greatly impact the return on investment. If that currency ’falls against the US dollar, it will lower the dollar value of the investment. And vice versa. (On the other hand, an increasing US dollar makes new purchases more attractive, making this a double-edged sword.)

Liquidity Risks

Foreign real estate is often less liquid than US real estate, making it hard to sell quickly without big losses. Market conditions, economic cycles, and local demand can all impact liquidity.

Investing in Overseas Property for Americans Afraid of US Market Chaos

Learn how investing in overseas property helps Americans escape US market chaos while avoiding reporting hassles. More information here: Investing in overseas property.

Frequently Asked Questions

What are the tax implications of owning foreign real estate in an IRA?

Foreign and domestic real estate in an IRA have the same US tax treatment. Income and gains are tax-deferred until you take distributions in a traditional IRA. All income or gains are tax-free in a Roth IRA.

But, if the property (domestic or foreign) is financed with debt, your IRA will need to pay Unrelated Business Income Tax (UBIT) on the debt-financed portion of the income or gain.

Can I live in or personally use the property I own through my IRA?

No. Doing so is a “prohibited transaction” and cause you to have to pay the full tax on the value of the IRA. If you’re under are 59½, there is also a 10% early withdrawal penalty.

How do currency fluctuations affect my real estate investment in an IRA?

Currency changes can significantly impact the value and returns of foreign real estate investments. If the US dollar strengthens against the currency where the property is located, it reduces the US dollar value of that property and the returns it generates. A weakening dollar would increase the relative value.

What happens if I want to sell the property?

Selling a property held in an IRA must be managed through the IRA, with all proceeds returning to the IRA to keep the tax benefits. IRS rules require all sales to be at arm’s length, meaning the property can’t be sold to a disqualified person (owner, owner’s family, or close friends.) The proceeds can be reinvested in other IRA-eligible assets or can stay in the IRA until distributions start.

Are there any countries that are more favorable for IRA real estate investments?

Certain countries offer better opportunities than others. But when we work with clients, we do not recommend getting into a local market you have no interest in and don’t want to get to know. Every market is unique and has unique quirks (including a legal system).

Buying real estate with IRAs: What are the complexities and compliance considerations?

Buying real estate with an IRA can offer long-term benefits—but it also comes with strict compliance requirements and potential pitfalls. We’ve covered the key rules, strategies, and mistakes to avoid in a dedicated article. Read more about buying real estate with an IRA here.

Need help?

Over the past 40+ years, we’ve helped thousands of clients build a better wealth protection plan. A good number of them have involved buying and selling foreign real estate.

Such investments can be quite exciting. But they can also be full of pitfalls without the right support.

If you’re thinking about buying real estate abroad and wondering which country is best for you, we can help. It starts with consultation with a Nestmann Associates to discuss your case. You can do that here.

About The Author

We have 40+ years experience helping Americans move, live and invest internationally…

Need Help?

We have 40+ years experience helping Americans move, live and invest internationally…