Negative Interest Rates and You

In August 2018, an astonishing $17 trillion in global debt had negative yields. About 30% of investment-grade bonds had yields below zero. If you bought these bonds and held them to maturity, you were guaranteed to lose money. Since then, the glut of bonds with negative yields has gone down by about $5 trillion. And that’s led to serious pain to anyone who bought them.

What are Negative Interest Rates?

Negative interest rates flip the usual rules of lending—borrowers get paid, not lenders.

Central banks use this unconventional monetary policy during severe economic downturns, charging commercial banks to hold reserves instead of crediting them. The goal is to push banks to lend more, encouraging spending and investment rather than letting cash sit idle and lose value.

The Global Shift to Negative Interest Rates and Its Impact on You

Interest rates throughout the world have been falling almost continuously since the 1980s.

- Sweden was the first country to impose negative interest rates on a consistent basis. It introduced a -0.25% rate on its “deposit interest rate” in 2009.

- The much larger European Central Bank (ECB), which sets monetary policy throughout the 19-country eurozone, followed suit in 2014 when it imposed a negative rate of -0.1%.

Negative interest rates were meant to be a temporary emergency measure to prop up struggling European economies. But they are also a great way for cash-strapped governments to pay the bills.

Switzerland was the first nation to issue long-term bonds with a negative yield. Its 10-year April 2025 bond was yielding -1.1% in mid-August 2019. As of this writing in November 2019, it now yields -0.4%. If you bought the bonds in August 2019 and hold them to maturity, your annual yield would be -1.1%. You could always sell them now, but if you did, you’d experience a substantial capital loss.

It’s easy to gloat at how the market has penalized investors who purchased these bonds. Yet it’s important to realize that you probably have more exposure to them than you might think. If you own a life insurance policy, are entitled to a pension, or invest in bond funds, you are likely more exposed to negative-yielding bonds than you realize.

Why Speculators Love Falling Interest Rates—and Why You Should Care

For most of us, the idea of accepting a small or even negative return on our investments is abhorrent. But bond speculators don’t care how low interest rates go, so long as they continue to fall. That’s because bond prices rise when interest rates fall, leading to profit opportunities. And the longer the duration of the bond, the more money they’ll make. This is because the longer a bond’s maturity, the more volatile its value is when interest rates change.

An example is the Austrian 100-year government bond, which matures in September 2117. As of this writing in November 2019, while this bond has a current yield of only 0.9%, its attraction to speculators is its duration. That’s because longer-term bonds are more sensitive to changes in interest rates than short-term bonds. In the case of the Austrian 100-year bond, its value changes by more than 70% for each 1% change in interest rates. So, while the bond was issued at a par value of 100, its value doubled within two years. A hedge fund operating with 5:1 leverage (i.e., with 80% borrowed money) which purchased this bond at par would have generated nearly a 500% profit.

However, the yield on this bond increased from 0.8% to 0.9% in the last few weeks. That meant the value of the bond decreased by around 7%. It will take nearly eight years to make up the difference unless long-term interest rates resume their fall. It would take a hedge fund purchasing this bond with 5:1 leverage 40 years to do so.

The Hidden Risks for Ordinary Investors—and How to Protect Yourself

But there’s a larger threat that’s less apparent. A decade of ultra-low to negative interest rates has resulted in an unprecedented search for yield by well-heeled investors, hedge funds, insurance companies, and pension funds. Trillions of dollars have flowed into bond funds, many of which are managed passively and tied to an index. That means ordinary investors—through their pension plans, insurance policies, and bond mutual funds—are unknowingly exposed to the risks of negative interest rate bonds.

Most of the time, the managers of index funds have an easy job; they merely need to buy the components of the index as money flows in. But what happens when index fund buyers start selling in droves? In that event, managers will have to do what they’ve promised: redeem investors’ holdings for cash. And they’ll need to sell in a hurry. This could turn into a vicious cycle where bonds must be liquidated at fire-sale prices, leading to catastrophic losses within days or even hours.

The Dangers of Passive Index Funds: Don’t Get Caught in the Stampede

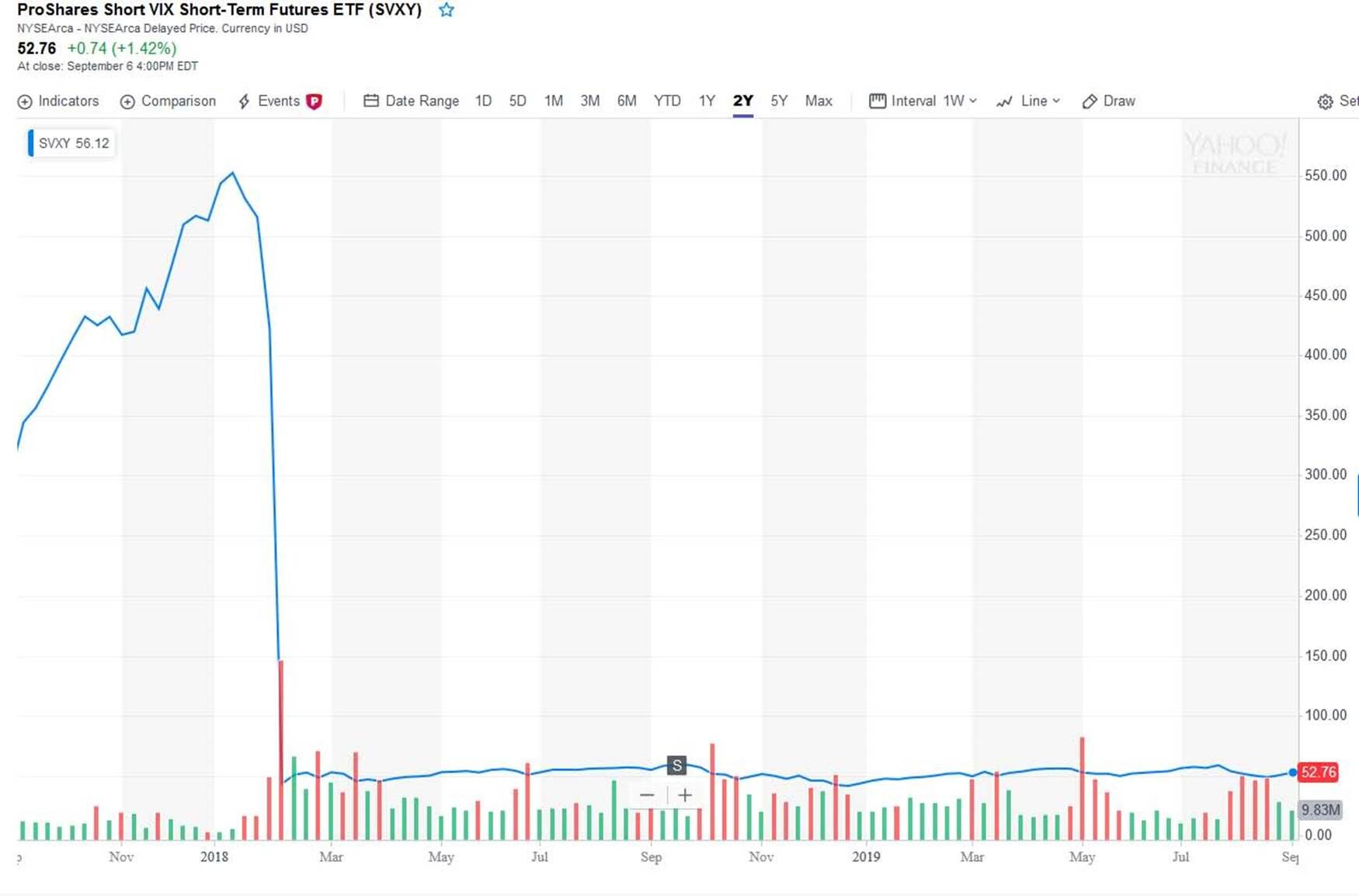

The danger of passive index funds is well-known but largely ignored. Occasionally, we get a reminder of what can happen when there’s a stampede out of an ETF. An example of this occurred in February 2018. At the time, there was great investor interest in the Chicago Board of Options Exchange Volatility Index (VIX). The VIX tends to spike in value during market selloffs, so it’s a popular way to profit in a financial crisis. Conversely, when markets are rising, the VIX decreases. Shorting the VIX can be very profitable in those times.

Thus, numerous ETFs were introduced to short the VIX. But in February 2018, during a market selloff, investor redemptions in funds that shorted the VIX led to a price meltdown in only a few days.

Here’s what happened to the value of ProShares Short VIX Short-Term Futures ETF (SVXY) during that period:

But the closest approximation we have predicts a grim result. In September 2019, a European regulator warned that 40% of European high-yield bond funds wouldn’t be able to meet even 10% of investor withdrawals in one week during a market shock.

How the Bond Bubble Could Burst—and What It Means for Your Wealth

Eventually, the gravy train will end. It must end because the biggest bond investors – hedge funds, insurance companies, and pension funds – won’t hold the bonds they own to maturity. If they do, the bonds will be redeemed at par value, and their premiums will evaporate. And the closer a bond gets to maturity, the lower the premium at which it trades. The only way to lock in profits is to sell the bonds many years before they mature.

But who will buy them when everyone is selling? Retail investors could be left holding the bag if institutional investors dump bonds. Hedge funds are also counting on central banks to intervene with new rounds of quantitative easing to prop up bond prices if mass selling begins.

That’s the exit strategy. But it might not work. If bond prices fall quickly enough once the selling begins, yields could rise very quickly. As September 2019’s European stress test demonstrated, only a small percentage of bond investors would realize their paper profits.

Could This Lead to a Global Financial Crisis?

Given ultra-high leverage, inflated bond prices, and the enormous size of the bond market, a sell-off could quickly trigger a global crisis paralyzing the financial markets. Central banks could try to quell it, but there’s no guarantee they will succeed.

My larger concern is that a bear market in bonds could turn into a systemic financial collapse. This is the term economists use for the collapse of an entire financial system. In that event, a loss in the value of your portfolio will be the least of your concerns. A more pressing issue could be that someone else has a superior claim to the assets you thought you owned.

For instance, you don’t own the assets in your bank account. The bank does. You have only a debt claim on those assets. Your legal status becomes that of an unsecured creditor holding an IOU. If the bank fails, and deposit insurance doesn’t pay up, you’re left holding the bag.

How to Protect Your Wealth from Negative Interest Rates

The only way to defend yourself from the systemic risks posed by negative interest rates is to ensure your assets are held by the safest and most liquid brokers or banks. Additionally, use strategies that position you at the front of the creditor line if those institutions fail.

And we can help you do just that. Since 1984, we’ve helped more than 15,000 customers and clients protect their wealth using proven, low-risk domestic and offshore planning. To see if our planning is right for you, please book an introductory consultation with one of our Associates.